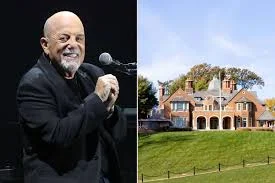

Billy Joel’s Waterfront Long Island Estate Was Finally Sold for $38 Million — A $14 Million Puzzle

SHOCK OPENING: The headline price reads $38, 000, 000, but documented component sales add up differently — a gap of roughly $2. 25 million to $14 million depending on which figures are counted. The discrepancy reframes what looked like a clean, headline-grabbing exit: billy joel’s long-gestating Centre Island compound was dismantled and sold in parts after nearly three years on the market.

What is not being told about the price and the pieces?

Verified facts: The estate first appeared for sale at $49 million in 2023, was taken off market for an extensive renovation, then relisted in 2024 at $49. 9 million. After failing to sell at that price, the property was parceled out: a seven-bedroom, nine-bathroom gatehouse sold for $7 million; the main brick manor moved for $23. 2 million; and two adjoining lots sold for $2. 75 million each — component sums that equal $35. 75 million. Emmett Laffey of Berkshire Hathaway HomeServices Laffey International Realty represented the seller and is credited with brokering what has been described as the priciest residential transaction on Long Island outside of the region commonly associated with the Hamptons.

Analysis: Those figures expose a fundamental tension between headline valuations and realized receipts. The initial expectations embedded in a $49–49. 9 million price tag never matched buyer demand; the estate’s deconstruction into discrete transactions produced a lower aggregate than the marquee asking price implied. The presence of differing totals — $38 million in some summaries versus $35. 75 million when adding reported components — leaves an unresolved accounting question about how public tallies are being presented and reconciled.

Who benefited and who bore the costs of breaking the estate apart?

Verified facts: The compound, assembled beginning with a bulk purchase in 2002 for $22. 5 million and expanded through additional adjoining parcels, ultimately comprised roughly 26 acres and roughly 2, 000 feet of private shoreline. The principal dwelling, completed in the early 1990s and known as MiddleSea, contains roughly 20, 000 square feet and numerous high-end amenities. Public details also show the estate carried an annual property tax burden that eclipsed $567, 000 — a factor cited in discussions about the decision to sell.

Analysis: Breaking the estate into sellable elements captured buyers interested in discrete assets — a separate gatehouse, individual lots, and the main manor — while converting a long-held, consolidated asset into more liquid pieces. Short-term winners include the purchasers of specialty components; longer-term costs include transaction expenses, renovation outlays, and the loss of the compound’s aggregated premium relative to a single-sale outcome. Emmett Laffey’s role as the agent frames the outcome as a market-driven compromise between what the seller sought and what buyers would pay.

What does the sale mean for billy joel and for Long Island property narratives?

Verified facts: The principal residence that carried the MiddleSea name and extensive waterfront amenities was sold in parts after almost three years of marketing and renovation. The owner continues to hold other properties in the region, indicating a continued presence in the state.

Analysis: This sequence — long listing, expensive renovation, and ultimately a piecemeal disposition — suggests a recalibration of expectations for trophy waterfront parcels outside high-demand seasonal enclaves. For billy joel, the transaction appears less like a definitive exit and more like a strategic reshaping of holdings in response to carrying costs and market appetite. For the public interest, the differing totals and the decision to sell by pieces highlight the need for clearer public accounting of multi-parcel luxury dispositions and the tax implications that drive them.

Accountability and next steps: Transparent reconciliation of headline totals with itemized sale components would clarify the public record. Municipal property records and transaction disclosures can close the remaining arithmetic gap and show how carrying costs, renovations, and staged sales affected final receipts for billy joel.